Causal Inference:

The Mixtape.

Buy the print version today:

Buy the print version today:

\[ % Define terms \newcommand{\Card}{\text{Card }} \DeclareMathOperator*{\cov}{cov} \DeclareMathOperator*{\var}{var} \DeclareMathOperator{\Var}{Var\,} \DeclareMathOperator{\Cov}{Cov\,} \DeclareMathOperator{\Prob}{Prob} \newcommand{\independent}{\perp \!\!\! \perp} \DeclareMathOperator{\Post}{Post} \DeclareMathOperator{\Pre}{Pre} \DeclareMathOperator{\Mid}{\,\vert\,} \DeclareMathOperator{\post}{post} \DeclareMathOperator{\pre}{pre} \]

Just as Archimedes said, “Give me a fulcrum, and I shall move the world,” you could just as easily say that with a good-enough instrument, you can identify any causal effect. But, while that is hyperbole, for reasons we will soon see, it is nonetheless the case that the instrumental variables (IV) design is potentially one of most important research designs ever devised. It is also unique because it is one of those instances that the econometric estimator was not simply ripped off from statistics (e.g., Eicker-Huber-White standard errors) or imported from some other field (e.g., like regression discontinuity). IV was invented by an economist, and its history is fascinating.

Philip Wright was born in 1861 and died in 1934. He received his bachelor’s degree from Tufts in 1884 and a master’s degree from Harvard in 1887. His son, Sewall Wright, was born in 1889 when Philip was 28. The family moved from Massachusetts to Galesburg, Illinois, where Philip took a position as professor of mathematics and economics at Lombard College. Philip published numerous articles and books in economics over his career, and he published poetry, too. You can see his vita here at https://scholar.harvard.edu/files/stock/files/wright_cv.jpg.1 Sewall attended Lombard College and took his college mathematics courses from his father.

In 1913, Philip took a position at Harvard, and Sewall entered there as a graduate student. Philip would later leave for the Brookings Institute, and Sewall would take his first job in the Department of Zoology at the University of Chicago, where he would eventually be promoted to professor in 1930.

Philip was prolific, which, given his sizable teaching and service requirements, is impressive. He published in top journals such as Quarterly Journal of Economics, Journal of the American Statistical Association, Journal of Political Economy, and American Economic Review. A common theme across many of his publications was the identification problem. He was acutely aware of it and intent on solving it.

In 1928, Philip was writing a book about animal and vegetable oils. The reason? He believed that recent tariff increases were harming international relations. And he wrote about the damage from the tariffs, which had affected animal and vegetable oils. The book, it turns out, would become a classic—not for tariffs or oils, but for being the first proof for the existence of an instrumental variables estimator.

While his father was publishing like a fiend in economics, Sewall Wright was revolutionizing the field of genetics. He invented path analysis, a precursor to Pearl’s directed acyclical graphic models, and he made important contributions to the theory of evolution and genetics. He was a genius. The decision to not follow in the family business (economics) created a bit of tension between the two men, but all evidence suggests that they found each other intellectually stimulating.

In his book on vegetable and oil tariffs, there is an appendix (entitled Appendix B) in which the calculus of an instrumental variables estimator was worked out. Elsewhere, Philip thanked his son for his valuable contributions to what he had written, referring to the path analysis that Sewall had taught him. This path analysis, it turned out, played a key role in Appendix B.

Appendix B showed a solution to the identification problem. So long as the economist is willing to impose some restrictions on the problem, then the system of equations can be identified. Specifically, if there is one instrument for supply, and the supply and demand errors are uncorrelated, then the elasticity of demand can be identified.

But who wrote this Appendix B? Either man could’ve done so. It is a chapter in an economics book, which points to Philip. But it used the path analysis, which points to Sewall. Historians have debated this, even going so far as to accuse Philip of stealing the idea from his son. If Philip stole the idea, by which I mean that when he published Appendix B, he failed to give proper attribution to his son, then it would at the very least have been a strange oversight. In come Stock and Trebbi (2003) to offer their opinions to this debate over authorship.

Stock and Trebbi (2003) tried to determine the authorship of Appendix B using “stylometric analysis.” Stylometric analysis had been used in other applications, such as to identify the author of the 1996 political novel Primary Colors (Joseph Klein) and the unsigned Federalist Papers. But Stock and Trebbi (2003) is easily the best application of stylometric analysis in economics.2

The method is akin to contemporary machine learning methods. The authors collected raw data containing the known original academic writings of each man, plus the first chapter and Appendix B of the book in question. All footnotes, graphs, and figures were excluded. Blocks of 1,000 words were selected from the files. Fifty-four blocks were selected: twenty written by Sewall with certainty, twenty-five by Philip, six from Appendix B, and three from chapter 1. Chapter 1 has always been attributed to Philip, but Stock and Trebbi (2003) treat the three blocks as unknown to check whether their model is correctly predicting authorship when authorship is already known.

The stylometric indicators that they used included the frequency of occurrence in each block of 70 function words. The list was taken from a separate study. These 70 function words produced 70 numerical variables, each of which is a count, per 1,000 words, of an individual function word in the block. Some words were dropped (e.g., “things” because they occurred only once), leaving 69 function words.

The second set of stylometric indicators, taken from another study, concerned grammatical constructions. Stock and Trebbi (2003) used 18 grammatical constructions, which were frequency counts. They included things like noun followed by an adverb, total occurrences of prepositions, coordinating conjunction followed by noun, and so on. There was one dependent variable in their analysis, and that was authorship. The independent variables were 87 covariates (69 function word counts and 18 grammatical statistics).

The results of this analysis are absolutely fascinating. For instance, many covariates have very large \(t\)-statistics, which would be unlikely if there really were no stylistic differences between the authors and the indicators were independently distributed.

So what do they find? Most interesting is their regression analysis. They write:

We regressed authorship against an intercept, the first two principal components of the grammatical statistics and the first two principal components of the function word counts, and we attribute authorship depending on whether the predicted value is greater or less than 0.5. (p.191)

And what did they find? That all of the Appendix B and chapter 1 blocks were assigned to Philip, not Sewall. They did other robustness checks, and all of them still pointed to Philip as the author.

Writing Appendix B and solving the problem that became Appendix B are technically distinct. But I nonetheless love this story for many reasons. First, I love the idea that an econometric estimator as important as instrumental variables has its roots in economics. I’m so accustomed to stories in which the actual econometric estimator was lifted from statistics (Huber-White standard errors) or educational psychology (regression discontinuity) that it’s nice to know economists have added their own designs to the canon. But the other part of the story that I love is the father-son component. It’s encouraging to know that a father and son can overcome differences through intellectual collaborations such as this. Such relationships are important, and tensions, when they arise, should be vigorously pursued until those tensions dissolve if possible. Relationships, and love more generally, matter after all. And Philip and Sewall give a story of that.

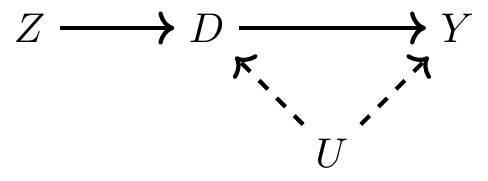

To understand the instrumental variables estimator, it is helpful to start with a DAG that shows a chain of causal effects that contains all the information needed to understand the instrumental variables strategy. First, notice the backdoor path between \(D\) and \(Y\): \(D \leftarrow U \rightarrow Y\). Furthermore, note that \(U\) is unobserved by the econometrician, which causes the backdoor path to remain open. If we have this kind of selection on unobservables, then there does not exist a conditioning strategy that will satisfy the backdoor criterion (in our data). But, before we throw up our arms, let’s look at how \(Z\) operates through these pathways.

First, there is a mediated pathway from \(Z\) to \(Y\) via \(D\). When \(Z\) varies, \(D\) varies, which causes \(Y\) to change. But, even though \(Y\) is varying when \(Z\) varies, notice that \(Y\) is only varying because \(D\) has varied. You sometimes hear people describe this as the “only through” assumption. That is, \(Z\) affects \(Y\) “only through” \(D\).

Imagine this for a moment though. Imagine \(D\) consists of people making choices. Sometimes these choices affect \(Y\), and sometimes these choices are merely correlated with changes in \(Y\) due to unobserved changes in \(U\). But along comes some shock, \(Z\), which induces some but not all of the people in \(D\) to make different decisions. What will happen?

Well, for one, when those people’s decisions change, \(Y\) will change too, because of the causal effect. But all of the correlation between \(D\) and \(Y\) in that situation will reflect the causal effect. The reason is that \(D\) is a collider along the backdoor path between \(Z\) and \(Y\).

But I’m not done with this metaphor. Let’s assume that in this \(D\) variable, with all these people, only some of the people change their behavior because of \(D\). What then? Well, in that situation, \(Z\) is causing a change in \(Y\) for just a subset of the population. If the instrument only changes the behavior of women, for instance, then the causal effect of \(D\) on \(Y\) will only reflect the causal effect of women’s choices, not men’s choices.

There are two ideas inherent in the previous paragraph that I want to emphasize. First, if there are heterogeneous treatment effects (e.g., men affect \(Y\) differently than women do), then our \(Z\) shock only identified some of the causal effect of \(D\) on \(Y\). And that piece of the causal effect may only be valid for the population of women whose behavior changed in response to \(Z\); it may not be reflective of how men’s behavior would affect \(Y\). And second, if \(Z\) is inducing some of the change in \(Y\) via only a fraction of the change in \(D\), then it’s almost as though we have less data to identify that causal effect than we really have.

Here we see two of the difficulties in interpreting instrumental variables and identifying a parameter using instrumental variables. Instrumental variables only identify a causal effect for any group of units whose behaviors are changed as a result of the instrument. We call this the causal effect of the complier population; in our example, only women “complied” with the instrument, so we only know its effect for them. And second, instrumental variables are typically going to have larger standard errors, and as such, they will fail to reject in many instances if for no other reason than being underpowered.

Moving along, let’s return to the DAG. Notice that we drew the DAG such that \(Z\) is independent of \(U\). You can see this because \(D\) is a collider along the \(Z \rightarrow D \leftarrow U\) path, which implies that \(Z\) and \(U\) are independent. This is called the “exclusion restriction,” which we will discuss in more detail later. But briefly, the IV estimator assumes that \(Z\) is independent of the variables that determine \(Y\) except for \(D\).

Second, \(Z\) is correlated with \(D\), and because of its correlation with \(D\) (and \(D\)’s effect on \(Y\)), \(Z\) is correlated with \(Y\) but only through its effect on \(D\). This relationship between \(Z\) and \(D\) is called the “first stage” because of the two-stage least squares estimator, which is a kind of IV estimator. The reason it is only correlated with \(Y\) via \(D\) is because \(D\) is a collider along the path \(Z\rightarrow D \leftarrow U \rightarrow Y\).

How do you know when you have a good instrument? One, it will require prior knowledge. I’d encourage you to write down that prior knowledge into a DAG and use it to reflect on the feasibility of your design. As a starting point, you can contemplate identifying a causal effect using IV only if you can theoretically and logically defend the exclusion restriction, since the exclusion restriction is an untestable assumption. That defense requires theory, and since some people aren’t comfortable with theoretical arguments like that, they tend to eschew the use of IV. More and more applied microeconomists are skeptical of IV because they are able to tell limitless stories in which exclusion restrictions do not hold.

But, let’s say you think you do have a good instrument. How might you defend it as such to someone else? A necessary but not sufficient condition for having an instrument that can satisfy the exclusion restriction is if people are confused when you tell them about the instrument’s relationship to the outcome. Let me explain. No one is likely to be confused when you tell them that you think family size will reduce the labor supply of women. They don’t need a Becker model to convince them that women who have more children probably are employed outside the home less often than those with fewer children.

But what would they think if you told them that mothers whose first two children were the same gender were employed outside the home less than those whose two children had a balanced sex ratio? They would probably be confused because, after all, what does the gender composition of one’s first two children have to do with whether a woman works outside the home? That’s a head scratcher. They’re confused because, logically, whether the first two kids are the same gender versus not the same gender doesn’t seem on its face to change the incentives a women has to work outside the home, which is based on reservation wages and market wages. And yet, empirically it is true that if your first two children are a boy, many families will have a third compared to those who had a boy and a girl first. So what gives?

The gender composition of the first two children matters for a family if they have preferences over diversity of gender. Families where the first two children were boys are more likely to try again in the hopes they’ll have a girl. And the same for two girls. Insofar as parents would like to have at least one boy and one girl, then having two boys might cause them to roll the dice for a girl.

And there you see the characteristics of a good instrument. It’s weird to a lay person because a good instrument (two boys) only changes the outcome by first changing some endogenous treatment variable (family size) thus allowing us to identify the causal effect of family size on some outcome (labor supply). And so without knowledge of the endogenous variable, relationships between the instrument and the outcome don’t make much sense. Why? Because the instrument is irrelevant to the determinants of the outcome except for its effect on the endogenous treatment variable. You also see another quality of the instrument that we like, which is that it’s quasi-random.

Before moving along, I’d like to illustrate this “weird instrument” in one more way, using two of my favorite artists: Chance the Rapper and Kanye West. At the start of this chapter, I posted a line from Kanye West’s wonderful song “Ultralight Beam” on the underrated Life of Pablo. On that song, Chance the Rapper sings:

I made “Sunday Candy,” I’m never going to hell.

I met Kanye West, I’m never going to fail.

Several years before “Ultralight Beam,” Chance made a song called “Sunday Candy.” It’s a great song and I encourage you to listen to it. But Chance makes a strange argument here on “Ultralight Beam.” He claims that because he made “Sunday Candy,” therefore he won’t go to hell. Now even a religious person will find that perplexing, as there is nothing in Christian theology of eternal damnation that would link making a song to the afterlife. This, I would argue, is a “weird instrument” because without knowing the endogenous variable on the mediated path \(SC \rightarrow ? \rightarrow H\), the two phenomena don’t seem to go together.

But let’s say that I told you that after Chance made “Sunday Candy,” he got a phone call from his old preacher. The preacher loved the song and invited Chance to come sing it at church. And while revisiting his childhood church, Chance had a religious experience that caused him to convert back to Christianity. Now, and only now, does his statement make sense. It isn’t that “Sunday Candy” itself shaped the path of his afterlife, so much as “Sunday Candy” caused a particular event that itself caused his beliefs about the future to change. That the line makes a weird argument is what makes “Sunday Candy” a good instrument.

But let’s take the second line—“I met Kanye West, I’m never going to fail.” Unlike the first line, this is likely not a good instrument. Why? Because I don’t even need to know what variable is along the mediated path \(KW \rightarrow ? \rightarrow F\) to doubt the exclusion restriction. If you are a musician, a relationship with Kanye West can possibly make or break your career. Kanye could make your career by collaborating with you on a song or by introducing you to highly talented producers. There is no shortage of ways in which a relationship with Kanye West can cause you to be successful, regardless of whatever unknown endogenous variable we have placed in this mediated path. And since it’s easy to tell a story where knowing Kanye West directly causes one’s success, knowing Kanye West is likely a bad instrument. It simply won’t satisfy the exclusion restriction in this context.

Ultimately, good instruments are jarring precisely because of the exclusion restriction—these two things (gender composition and work) don’t seem to go together. If they did go together, it would likely mean that the exclusion restriction was violated. But if they don’t, then the person is confused, and that is at minimum a possible candidate for a good instrument. This is the commonsense explanation of the “only through” assumption.

There are two ways to discuss the instrumental variables design: one in a world where the treatment has the same causal effect for everybody (“homogeneous treatment effects”) and one in a world where the treatment effects can differ across the population (“heterogeneous treatment effects”). For homogeneous treatment effects, I will depend on a more traditional approach rather than on potential outcomes notation. When the treatment effect is constant, I don’t feel we need potential outcomes notation as much.

Instrumental variables methods are typically used to address omitted variable bias, measurement error, and simultaneity. For instance, quantity and price is determined by the intersection of supply and demand, so any observational correlation between price and quantity is uninformative about the elasticities associated with supply or demand curves. Philip Wright understood this, which was why he investigated the problem so intensely.

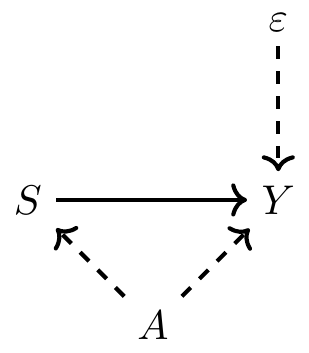

I will assume a homogeneous treatment effect of \(\delta\) which is the same for every person. This means that if college caused my wages to increase by 10%, it also caused your wages to increase by 10%. Let’s start by illustrating the problem of omitted variable bias. Assume the classical labor problem where we’re interested in the causal effect of schooling on earnings, but schooling is endogenous because of unobserved ability. Let’s draw a simple DAG to illustrate this setup.

We can represent this DAG with a simple regression. Let the true model of earnings be:

\[ \begin{align} Y_i = \alpha + \delta S_i + \gamma A_i + \varepsilon_i \end{align} \]

where \(Y\) is the log of earnings, \(S\) is schooling measured in years, \(A\) is individual “ability,” and \(\varepsilon\) is an error term uncorrelated with schooling or ability. The reason \(A\) is unobserved is simply because the surveyor either forgot to collect it or couldn’t collect it and therefore it’s missing from the data set.3 For instance, the CPS tells us nothing about respondents’ family background, intelligence, motivation, or non-cognitive ability. Therefore, since ability is unobserved, we have the following equation instead:

\[ \begin{align} Y_i = \alpha + \delta S_i + \eta_i \end{align} \]

where \(\eta_i\) is a composite error term equalling \(\gamma A_i + \varepsilon_i\). We assume that schooling is correlated with ability, so therefore it is correlated with \(\eta_i\), making it endogenous in the second, shorter regression. Only \(\varepsilon_i\) is uncorrelated with the regressors, and that is by definition.

We know from the derivation of the least squares operator that the estimated value of \(\widehat{\delta}\) is:

\[ \begin{align} \widehat{\delta} = \dfrac{C(Y,S)}{V(S)} = \dfrac{E[YS] - E[Y]E[S]}{V(S)} \end{align} \]

Plugging in the true value of \(Y\) (from the longer model), we get the following:

\[ \begin{align} \widehat{\delta} & = \dfrac{E\big[\alpha S + S^2 \delta + \gamma SA + \varepsilon S\big] - E(S)E\big[\alpha + \delta S + \gamma A + \varepsilon\big]}{V(S)} \\ & = \dfrac{ \delta E(S^2) - \delta E(S)^2 + \gamma E(AS) - \gamma E(S)E(A) + E(\varepsilon S) - E(S)E(\varepsilon)}{V(S)} \\ & = \delta + \gamma \dfrac{C(AS)}{V(S)} \end{align} \]

If \(\gamma>0\) and \(C(A,S)>0\), then \(\widehat{\delta}\), the coefficient on schooling, is upward biased. And that is probably the case given that it’s likely that ability and schooling are positively correlated.

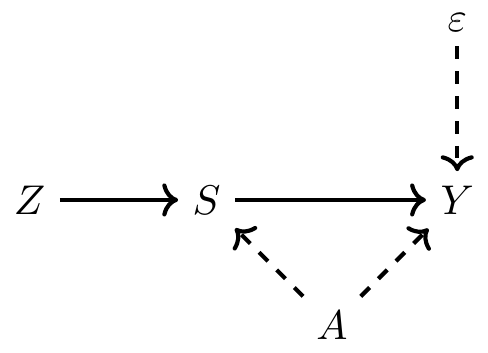

But let’s assume that you have found a really great weird instrument \(Z_i\) that causes people to get more schooling but that is independent of student ability and the structural error term. It is independent of ability, which means we can get around the endogeneity problem. And it’s not associated with the other unobserved determinants of earnings, which basically makes it weird. The DAG associated with this set up would look like this:

We can use this variable, as I’ll now show, to estimate \(\delta\). First, calculate the covariance of \(Y\) and \(Z\):

\[ \begin{align} C(Y,Z) & = C(\alpha + \delta S+\gamma A+\varepsilon, Z) \\ & = E\big[(\alpha+\delta S+\gamma A+\varepsilon),Z] - E(S) E(Z) \\ & =\big\{\alpha E(Z)- \alpha E(Z)\big\} + \delta \big\{E(SZ) - E(S)E(Z)\big\} \\ & \quad + \gamma \big\{E(AZ) - E(A)E(Z)\big\} + \big\{E(\varepsilon Z) - E(\varepsilon)E(Z)\big\} \\ & =\delta C(S,Z) + \gamma C(A,Z) + C(\varepsilon, Z) \end{align} \]

Notice that the parameter of interest, \(\delta\) is on the right side. So how do we isolate it? We can estimate it with the following:

\[ \begin{align} \widehat{\delta} = \dfrac{C(Y,Z)}{C(S,Z)} \end{align} \]

so long as \(C(A,Z)=0\) and \(C(\varepsilon,Z)=0\).

These zero covariances are the statistical truth contained in the IV DAG from earlier. If ability is independent of \(Z\), then this second covariance is zero. And if \(Z\) is independent of the structural error term, \(\varepsilon\), then it too is zero. This, you see, is what is meant by the “exclusion restriction”: the instrument must be independent of both parts of the composite error term.

But the exclusion restriction is only a necessary condition for IV to work; it is not a sufficient condition. After all, if all we needed was exclusion, then we could use a random number generator for an instrument. Exclusion is not enough. We also need the instrument to be highly correlated with the endogenous variable schooling \(S\). And the higher the better. We see that here because we are dividing by \(C(S,Z)\), so it necessarily requires that this covariance not be zero.

The numerator in this simple ratio is sometimes called the “reduced form,” while the denominator is called the “first stage.” These terms are somewhat confusing, particularly the former, as “reduced form” means different things to different people. But in the IV terminology, it is that relationship between the instrument and the outcome itself. The first stage is less confusing, as it gets its name from the two-stage least squares estimator, which we’ll discuss next.

When you take the probability limit of this expression, then assuming \(C(A,Z)=0\) and \(C(\varepsilon , Z)=0\) due to the exclusion restriction, you get \[ p\lim\ \widehat{\delta} = \delta \] But if \(Z\) is not independent of \(\eta\) (either because it’s correlated with \(A\) or \(\varepsilon\)), and if the correlation between \(S\) and \(Z\) is weak, then \(\widehat{\delta}\) becomes severely biased in finite samples.

One of the more intuitive instrumental variables estimators is the two-stage least squares (2SLS). Let’s review an example to illustrate why it is helpful for explaining some of the IV intuition. Suppose you have a sample of data on \(Y\), \(S\), and \(Z\). For each observation \(i\), we assume the data are generated according to:

\[ \begin{align} Y_i & = \alpha + \delta S_i + \varepsilon_i \\ S_i & = \gamma + \beta Z_i + \epsilon_i \end{align} \]

where \(C(Z,\varepsilon)=0\) and \(\beta \neq 0\). The former assumption is the exclusion restriction whereas the second assumption is a non-zero first-stage. Now using our IV expression, and using the result that \(\sum_{i=1}^n(x_i -\bar{x})=0\), we can write out the IV estimator as:

\[ \begin{align} \widehat{\delta} & = \dfrac{C(Y,Z)}{C(S,Z)} \\ & = \dfrac{ \dfrac{1}{n} \sum_{i=1}^n (Z_i - \overline{Z})(Y_i - \overline{Y}) }{ \dfrac{1}{n} \sum_{i=1}^n (Z_i - \overline{Z}) (S_i - \overline{S})} \\ & =\dfrac{ \dfrac{1}{n} \sum_{i=1}^n (Z_i - \overline{Z})Y_i}{ \dfrac{1}{n} \sum_{i=1}^n (Z_i -\overline{Z})S_i} \end{align} \]

When we substitute the true model for \(Y\), we get the following:

\[ \begin{align} \widehat{\delta} & =\dfrac{ \dfrac{1}{n} \sum_{i=1}^n (Z_i - \overline{Z})\{\alpha + \delta S + \varepsilon \}}{\dfrac{1}{n} \sum_{i=1}^n (Z_i - \overline{Z})S_i} \\ & =\delta + \dfrac{ \dfrac{1}{n} \sum_{i=1}^n (Z_i - \overline{Z})\varepsilon_i}{ \dfrac{1}{n} \sum_{i=1}^n (Z_i - \overline{Z})S_i } \\ & =\delta + \text{``small if $n$ is large''} \end{align} \]

So, let’s return to our first description of \(\widehat{\delta}\) as the ratio of two covariances. With some simple algebraic manipulation, we get the following:

\[ \begin{align} \widehat{\delta} & =\dfrac{ C(Y,Z)}{C(S,Z)} \\ & =\dfrac{ \dfrac{C(Z,Y)}{V(Z)} }{\dfrac{ C(Z,S)}{V(Z)}} \end{align} \]

where the denominator is equal to \(\widehat{\beta}\).4 We can rewrite \(\widehat{\beta}\) as:

\[ \begin{align} \widehat{\beta} & = \dfrac{ C(Z,S)}{V(Z)} \\ \widehat{\beta}V(Z) & =C(Z,S) \end{align} \]

Then we rewrite the IV estimator and make a substitution:

\[ \begin{align} \widehat{\delta}_{IV} & =\dfrac{ C(Z,Y)}{C(Z,S)} \\ & =\dfrac{\widehat{\beta}C(Z,Y)}{\widehat{\beta} C(Z,S)} \\ & =\dfrac{ \widehat{\beta} C(Z,Y)}{\widehat{\beta}^2 V(Z)} \\ & = \dfrac{C(\widehat{\beta}Z,Y)}{V(\widehat{\beta}Z)} \end{align} \]

Notice now what is inside the parentheses: \(\widehat{\beta}Z\), which are the fitted values of schooling from the first-stage regression. We are no longer, in other words, using \(S\)—we are using its fitted values. Recall that \(S=\gamma + \beta Z + \epsilon\); \(\widehat{\delta} = \dfrac{ C(\widehat{\beta}ZY)}{V(\widehat{\beta}Z)}\) and let \(\widehat{S} = \widehat{\gamma} + \widehat{\beta}Z\). Then the two-stage least squares (2SLS) estimator is:

\[ \begin{align} \widehat{\delta}_{IV} & = \dfrac{ C(\widehat{\beta}Z,Y)}{V(\widehat{\beta}Z)} \\ & =\dfrac{C(\widehat{S},Y)}{V(\widehat{S})} \end{align} \]

I will now show that \(\widehat{\beta}C(Y,Z)=C(\widehat{S},Y)\), and leave it to you to show that \(V(\widehat{\beta}Z)=V(\widehat{S})\).

\[ \begin{align} C(\widehat{S},Y) & = E[\widehat{S}Y] - E[\widehat{S}]E[Y] \\ & = E\Big(Y[\widehat{\gamma}+\widehat{\beta}Z]\Big) - E(Y)E(\widehat{\gamma} + \widehat{\beta}Z) \\ & =\widehat{\gamma}E(Y) + \widehat{\beta}E(YZ) - \widehat{\gamma}E(Y) - \widehat{\beta}E(Y)E(Z) \\ & =\widehat{\beta}\big[E(YZ)-E(Y)E(Z)\big] \\ C(\widehat{S},Y) & = \widehat{\beta}C(Y,Z) \end{align} \]

Now let’s return to something I said earlier—learning 2SLS can help you better understand the intuition of instrumental variables more generally. What does this mean exactly? First, the 2SLS estimator used only the fitted values of the endogenous regressors for estimation. These fitted values were based on all variables used in the model, including the excludable instrument. And as all of these instruments are exogenous in the structural model, what this means is that the fitted values themselves have become exogenous too. Put differently, we are using only the variation in schooling that is exogenous. So that’s kind of interesting, as now we’re back in a world where we are identifying causal effects from exogenous changes in schooling caused by our instrument.

But, now the less-exciting news. This exogenous variation in \(S\) driven by the instrument is only a subset of the total variation in schooling. Or put differently, IV reduces the variation in the data, so there is less information available for identification, and what little variation we have left comes from only those units who responded to the instrument in the first place. This, it turns out, will be critical later when we relax the homogeneous treatment effects assumption and allow for heterogeneity.

It’s helpful to occasionally stop and try to think about real-world applications as much as possible; otherwise the estimators feel very opaque and unhelpful. So to illustrate, I’m going to review one of my own papers with Keith Finlay that sought to estimate the effect that parental methamphetamine abuse had on child abuse and foster care admissions (Cunningham and Finlay 2012).

It has been claimed that substance abuse, notably illicit drug use, has a negative impact on parenting, causing neglect, but as these all occur in equilibrium, it’s possible that the correlation is simply reflective of selection bias. Maybe households with parents who abuse drugs would’ve had the same negative outcomes had the parents not used drugs. After all, it’s not like people are flipping coins when deciding to smoke meth. So let me briefly give you some background to the study so that you better understand the data-generating process.

First, methamphetamine is a toxic poison to the mind and body and highly addictive. Some of the symptoms of meth abuse are increased energy and alertness, decreased appetite, intense euphoria, impaired judgment, and psychosis. Second, the meth epidemic in the United States began on the West Coast, before gradually making its way eastward over the 1990s.

We were interested in the impact that this growth in meth abuse was having on children. Observers and law enforcement had commented, without concrete causal evidence, that the epidemic was causing a growth in foster care admissions. But how could we separate correlation from causality? The solution was contained within how meth itself is produced.

Meth is synthesized from a reduction of ephedrine or pseudoephedrine, which is also the active ingredient in many cold medications, such as Sudafed. Without one of these two precursors, it is impossible to produce the kind of meth people abuse. These precursors had supply chains that could be potentially disrupted because of the concentration of pharmaceutical laboratories. In 2004, nine factories manufactured the bulk of the world’s supply of ephedrine and pseudoephedrine. The US Drug Enforcement Agency correctly noted that if it could regulate access to ephedrine and pseudoephedrine, then it could effectively interrupt the production of methamphetamine, and in turn, hypothetically reduce meth abuse and its associated social harms.

So, with input from the DEA, Congress passed the Domestic Chemical Diversion Control Act in August 1995, which provided safeguards by regulating the distribution of products that contained ephedrine as the primary medicinal ingredient. But the new legislation’s regulations applied to ephedrine, not pseudoephedrine, and since the two precursors were nearly identical, traffickers quickly substituted. By 1996, pseudoephedrine was found to be the primary precursor in almost half of meth lab seizures.

Therefore, the DEA went back to Congress, seeking greater control over pseudoephedrine products. And the Comprehensive Methamphetamine Control Act of 1996 went into effect between October and December 1997. This act required distributors of all forms of pseudoephedrine to be subject to chemical registration. Dobkin and Nicosia (2009) argued that these precursor shocks may very well have been the largest supply shocks in the history of drug enforcement.

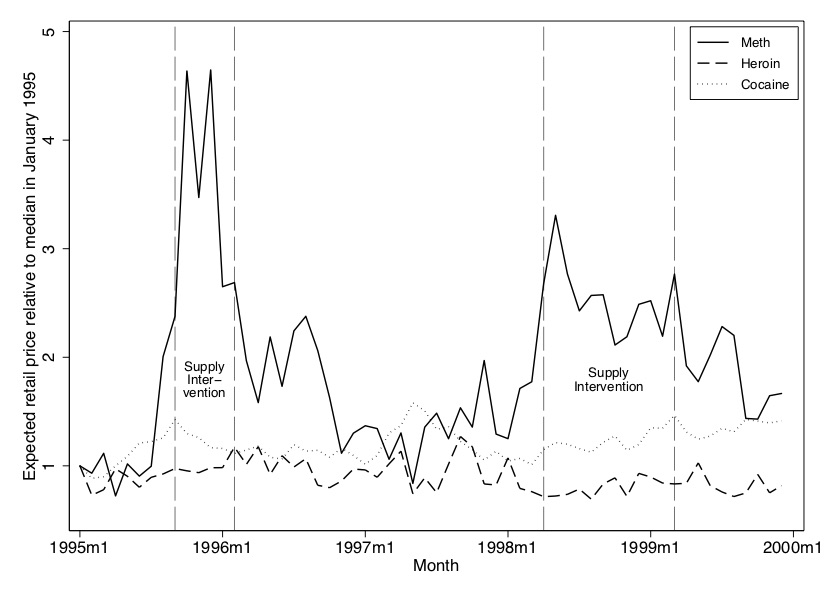

We placed a Freedom of Information Act request with the DEA requesting all of their undercover purchases and seizures of illicit drugs going back decades. The data included the price of an undercover purchase, the drug’s type, its weight and its purity, as well as the locations in which the purchases occurred. We used these data to construct a price series for meth, heroin, and cocaine. The effect of the two interventions were dramatic. The first supply intervention caused retail (street) prices (adjusted for purity, weight, and inflation) to more than quadruple. The second intervention, while still quite effective at raising relative prices, did not have as large an effect as the first. See Figure 7.1.

We showed two other drug prices (cocaine and heroin) in addition to meth because we wanted the reader to understand that the 1995 and 1997 shocks were uniquely impacting meth markets. They did not appear to be common shocks affecting all drug markets, in other words. As a result, we felt more confident that our analysis would be able to isolate the effect of methamphetamine, as opposed to substance abuse more generally. The two interventions simply had no effect on cocaine and heroin prices despite causing a massive shortage of meth and raising its retail price. It wouldn’t have surprised me if disrupting meth markets had caused a shift in demand for cocaine or heroin and in turn caused its prices to change, yet at first glance in the time series, I’m not finding that. Weird.

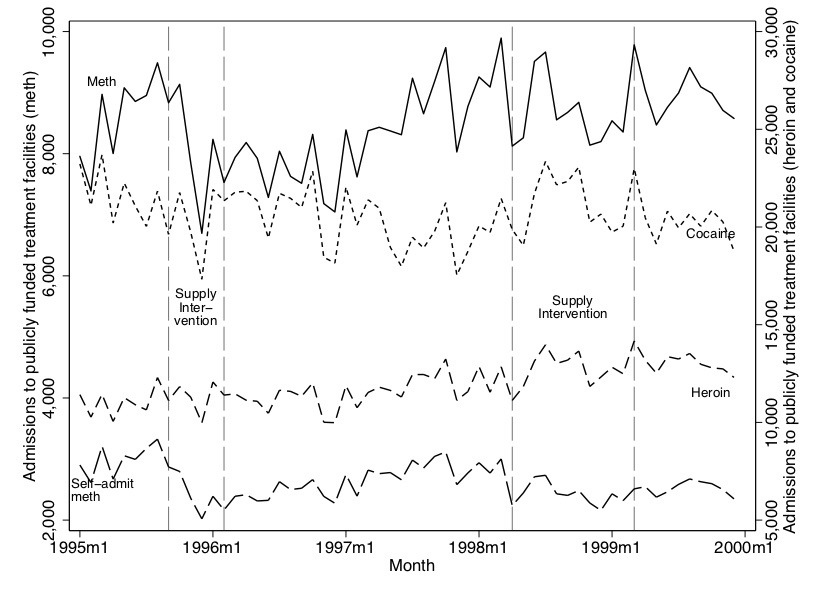

We are interested in the causal effect of meth abuse on child abuse, and so our first stage is necessarily a proxy for meth abuse—the number of people entering treatment who listed meth as one of the substances they used in their last episode of substance abuse. As I said before, since a picture is worth a thousand words, I’m going to show you pictures of both the first stage and the reduced form. Why do I do this instead of going directly to the tables of coefficients? Because quite frankly, you are more likely to find those estimates believable if you can see evidence for the first stage and the reduced form in the raw data itself.5

In Figure 7.2, we show the first stage. All of these data come from the Treatment Episode Data Set (TEDS), which includes all people going into treatment for substance abuse at federally funded clinics. Patients list the last three substances used in the most recent “episode.” We mark anyone who listed meth, cocaine, or heroin and aggregate by month and state. But first, let’s look at the national aggregate in Figure 7.2. You can see evidence for the effect the two interventions had on meth flows, particularly the ephedrine intervention. Self-admitted meth admissions dropped significantly, as did total meth admissions, but there’s no effect on cocaine or heroin. The effect of the pseudoephedrine is not as dramatic, but it appears to cause a break in trend as the growth in meth admissions slows during this period of time. In summary, it appears we have a first stage because, during the interventions, meth admissions declines.

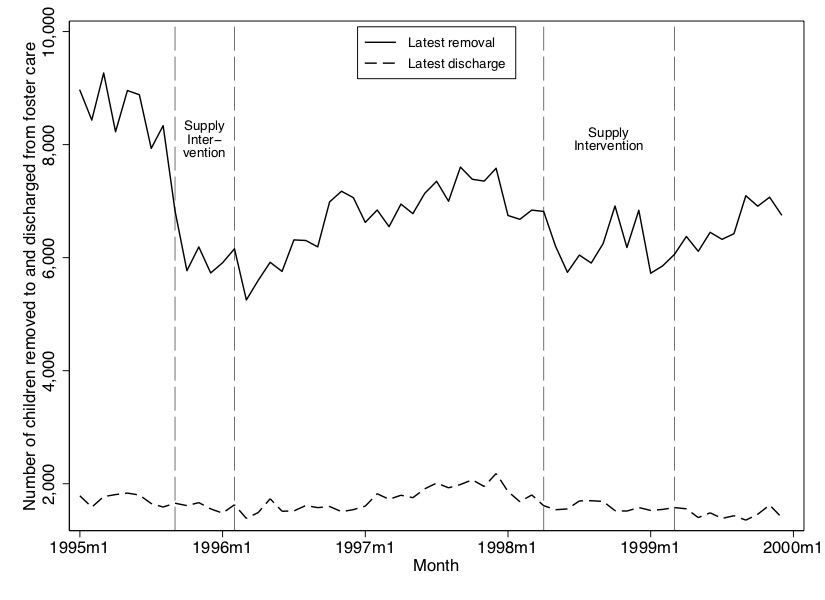

In Figure 7.3, we show the reduced form—that is, the effect of the price shocks on foster care admissions. Consistent with what we found in our first-stage graphic, the ephedrine intervention in particular had a profoundly negative effect on foster care admissions. They fell from around 8,000 children removed per month to around 6,000, then began rising again. The second intervention also had an effect, though it appears to be milder. The reason we believe that the second intervention had a more modest effect than the first is because (1) the effect on price was about half the size of the first intervention, and (2) domestic meth production was being replaced by Mexican imports of meth over the late 1990s, and the precursor regulations were not applicable in Mexico. Thus, by the end of the 1990s, domestic meth production played a smaller role in total output, and hence the effect on price and admissions was probably smaller.

It’s worth reflecting for a moment on the reduced form. Why would rising retail prices of a pure gram of methamphetamine cause a child not to be placed in foster care? Prices don’t cause child abuse—they’re just nominal pieces of information in the world. The only way in which a higher price for meth could reduce foster care admissions is if parents reduced their consumption of methamphetamine, which in turn caused a reduction in harm to one’s child. This picture is a key piece of evidence for the reader that this is going on.

In Table 7.1, I reproduce our main results from my article with Keith. There are a few pieces of key information that all IV tables should have. First, there is the OLS regression. As the OLS regression suffers from endogeneity, we want the reader to see it so that they have something to compare the IV model to. Let’s focus on column 1, where the dependent variable is total entry into foster care. We find no effect, interestingly, of meth on foster care when we estimate using OLS.

| Log Latest Entry into Foster Care | Log Latest Entry into Child Neglect | Log Latest Entry into Physical Abuse | ||||

|---|---|---|---|---|---|---|

| Covariates | OLS | 2SLS | OLS | 2SLS | OLS | 2SLS |

| Log self-referred | 0.001 | 1.54\(^{***}\) | 0.03 | 1.03\(^{***}\) | 0.04 | 1.49\(^{**}\) |

| Meth treatment rate | (0.02) | (0.59) | (0.02) | (0.41) | (0.03) | (0.62) |

| Month-of-year fixed effects | Yes | Yes | Yes | Yes | Yes | Yes |

| State controls | Yes | Yes | Yes | Yes | Yes | Yes |

| State fixed effects | Yes | Yes | Yes | Yes | Yes | Yes |

| State linear time trends | Yes | Yes | Yes | Yes | Yes | Yes |

| First Stage Instrument | ||||||

| Price deviation instrument | \(-0.0005^{***}\) | \(-0.0005^{***}\) | \(-0.0005^{**}\) | |||

| (0.0001) | (0.0001) | (0.0001) | ||||

| \(F\)-statistic for IV in first stage | 17.60 | 17.60 | 17.60 | |||

| \(N\) | 1,343 | 1,343 | 1,343 | 1,343 |

Notes: Log latest entry into foster care is the natural log of the sum of all new foster care admissions by state, race, and month. Models 3 to 10 denote the flow of children into foster care via a given route of admission denoted by the column heading. Models 11 and 12 use the natural log of the sum of all foster care exits by state, race and month. \(^{***}\), \(^{**}\), and \(^{*}\) denote statistical significance at the 1%, 5%, and 10% levels, respectively.

The second piece of information that one should report in a 2SLS table is the first stage itself. We report the first stage at the bottom of each even-numbered column. As you can see, for each one-unit deviation in price from its long-term trend, meth admissions into treatment (our proxy) fell by \(-0.0005\) log points. This is highly significant at the 1% level, but we check for the strength of the instrument using the \(F\) statistic (Staiger and Stock 1997).6 We have an \(F\) statistic of 17.6, which suggests that our instrument is strong enough for identification.

Finally, let’s examine the 2SLS estimate of the treatment effect itself. Notice using only the exogenous variation in log meth admissions, and assuming the exclusion restriction holds in our model, we are able to isolate a causal effect of log meth admissions on log aggregate foster care admissions. As this is a log-log regression, we can interpret the coefficient as an elasticity. We find that a 10% increase in meth admissions for treatment appears to cause around a 15% increase in children being removed from their homes and placed into foster care. This effect is both large and precise. And it was not detectable otherwise (the coefficient was zero).

Why are they being removed? Our data (AFCARS) lists several channels: parental incarceration, child neglect, parental drug use, and physical abuse. Interestingly, we do not find any effect of parental drug use or parental incarceration, which is perhaps counterintuitive. Their signs are negative and their standard errors are large. Rather, we find effects of meth admissions on removals for physical abuse and neglect. Both are elastic (i.e., \(\delta >1\)).

What did we learn? First, we learned how a contemporary piece of applied microeconomics goes about using instrumental variables to identify causal effects. We saw the kinds of graphical evidence mustered, the way in which knowledge about the natural experiment and the policies involved helped the authors argue for the exclusion restriction (since it cannot be tested), and the kind of evidence presented from 2SLS, including the first-stage tests for weak instruments. Hopefully seeing a paper at this point was helpful. But the second thing we learned concerned the actual study itself. We learned that for the group of meth users whose behavior was changed as a result of rising real prices of a pure gram of methamphetamine (i.e., the complier subpopulation), their meth use was causing child abuse and neglect so severe that it merited removing their children and placing those children into foster care. If you were only familiar with Dobkin and Nicosia (2009), who found no effect of meth on crime using county-level data from California and only the 1997 ephedrine shock, you might incorrectly conclude that there are no social costs associated with meth abuse. But, while meth does not appear to cause crime in California, it does appear to harm the children of meth users and places strains on the foster care system.

I am not trying to smother you with papers. But before we move back into the technical material itself, I’d like to discuss one more paper. This paper will also help you better understand the weak instrument literature following its publication.

As we’ve said since the beginning, with example after example, there is a very long tradition in labor economics of building models that can credibly identify the returns to schooling. This goes back to Becker (1994) and the workshop at Columbia that Becker ran for years with Jacob Mincer. This study of the returns to schooling has been an important task given education’s growing importance in the distribution of income and wealth since the latter twentieth century with increasing returns to skill in the marketplace (Juhn, Murphy, and Pierce 1993).

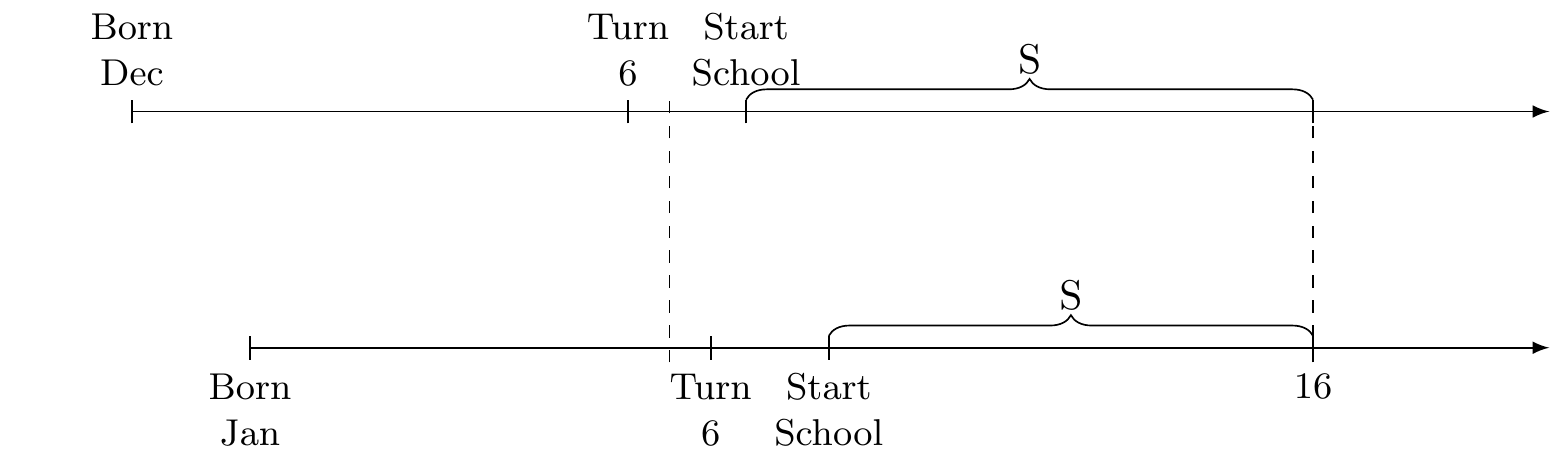

One of the more seminal papers in instrumental variables for the modern period is Angrist and Krueger (1991). Their idea is simple and clever; a quirk in the United States educational system is that a child enters a grade on the basis of his or her birthday. For a long time, that cutoff was late December. If children were born on or before December 31, then they were assigned to the first grade. But if their birthday was on or after January 1, they were assigned to kindergarten. Thus two people—one born on December 31 and one born on January 1—were exogenously assigned different grades.

Now there’s nothing necessarily relevant here because if those children always stay in school for the duration necessary to get a high school degree, then that arbitrary assignment of start date won’t affect high school completion. It’ll only affect when they get that high school degree. But this is where it gets interesting. For most of the twentieth century, the US had compulsory schooling laws that forced a person to remain in high school until age 16. After age 16, one could legally stop going to school. Figure 7.4 explains visually this instrumental variable.7

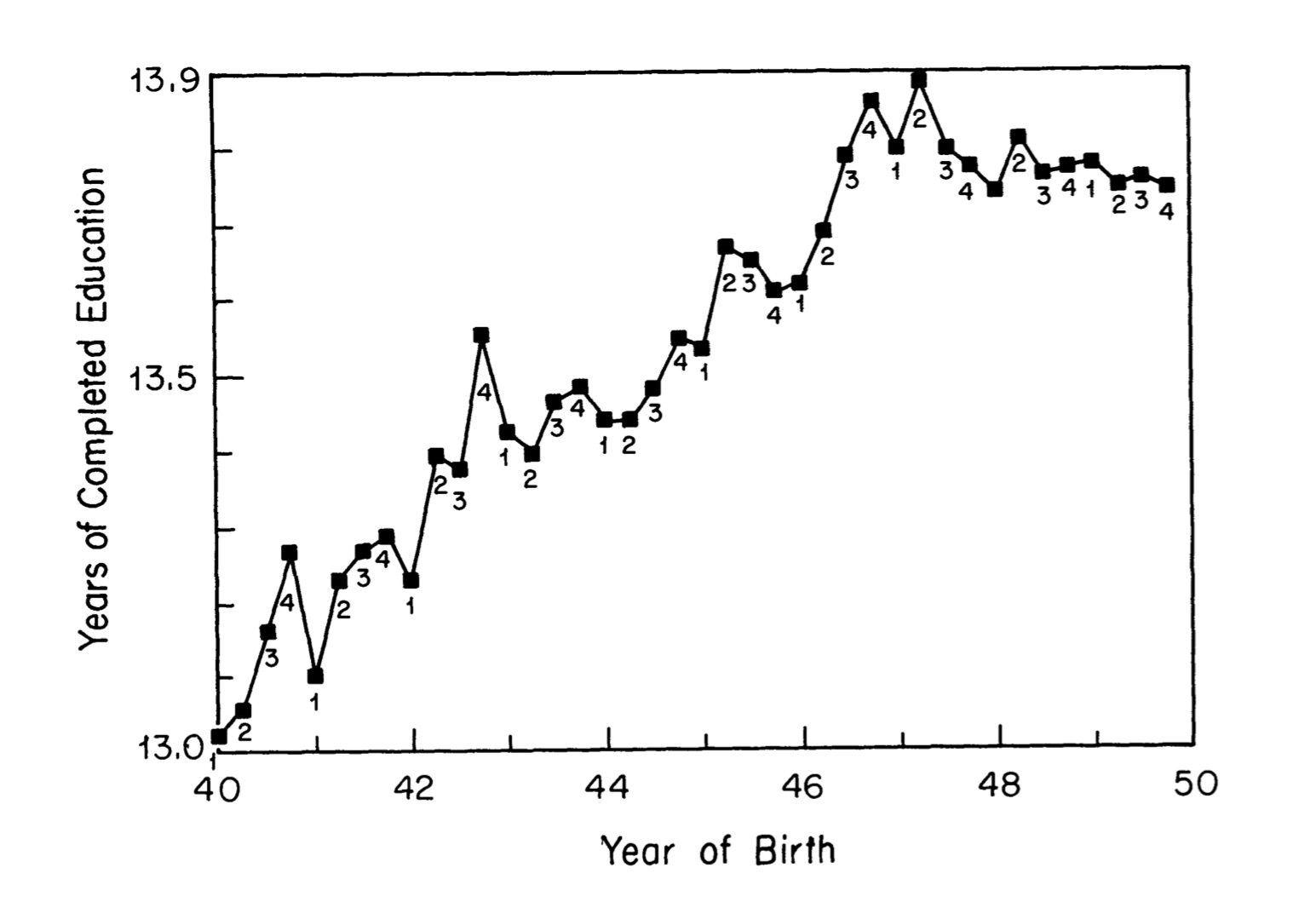

Angrist and Krueger had the insight that that small quirk was exogenously assigning more schooling to people born later in the year. The person born in December would reach age 16 with more education than the person born in January, in other words. Thus, the authors uncovered small exogenous variation in schooling. Notice how similar their idea was to regression discontinuity. That’s because IV and RDD are conceptually very similar strategies.

Figure 7.5 shows the first stage, and it is really interesting. Look at all those 3s and 4s at the top of the picture. There’s a clear pattern—those with birthdays in the third and fourth quarter have more schooling on average than do those with birthdays in the first and second quarters. That relationship gets weaker as we move into later cohorts, but that is probably because for later cohorts, the price on higher levels of schooling was rising so much that fewer and fewer people were dropping out before finishing their high school degree.

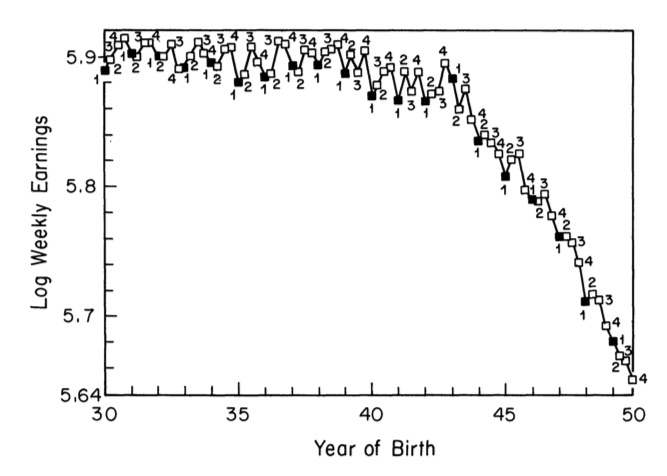

Figure 7.6 shows the reduced-form relationship between quarter of birth and log weekly earnings.8 You have to squint a little bit, but you can see the pattern—all along the top of the jagged path are 3s and 4s, and all along the bottom of the jagged path are 1s and 2s. Not always, but it’s correlated.

Remember what I said about how instruments having a certain ridiculousness to them? That is, you know you have a good instrument if the instrument itself doesn’t seem relevant for explaining the outcome of interest because that’s what the exclusion restriction implies. Why would quarter of birth affect earnings? It doesn’t make any obvious, logical sense why it should. But, if I told you that people born later in the year got more schooling than those with less because of compulsory schooling, then the relationship between the instrument and the outcome snaps into place. The only reason we can think of as to why the instrument would affect earnings is if the instrument were operating through schooling. Instruments only explain the outcome, in other words, when you understand their effect on the endogenous variable.9

Angrist and Krueger use three dummies as their instruments: a dummy for first quarter, a dummy for second quarter, and a dummy for third quarter. Thus, the omitted category is the fourth quarter, which is the group that gets the most schooling. Now ask yourself this: if we regressed years of schooling onto those three dummies, what should the signs and magnitudes be? That is, what would we expect the relationship between the first quarter (compared to the fourth quarter) and schooling? Let’s look at their first-stage results (Table 7.2).

| Quarter of Birth Effect | ||||

| Outcome variable | Birth Cohort | I | II | III |

| Total schooling | 1930-1939 | -0.124 | -0.86 | -0.015 |

| (0.017) | (0.017) | (0.016) | ||

| 1940–1949 | \(-0.085\) | \(-0.035\) | \(-0.017\) | |

| (0.012) | (0.012) | (0.011) | ||

| High school grad | 1930-1939 | \(-0.019\) | \(-0.020\) | \(-0.004\) |

| (0.002) | (0.002) | (0.002) | ||

| 1940–1949 | \(-0.015\) | \(-0.012\) | \(-0.002\) | |

| (0.001) | (0.001) | (0.001) | ||

| College grad | 1930-1939 | \(-0.005\) | 0.003 | 0.002 |

| (0.002) | (0.002) | (0.002) | ||

| 1940–1949 | \(-0.003\) | 0.004 | 0.000 | |

| (0.002) | (0.002) | (0.002) |

Standard errors in parenthesis.

Table 7.2 shows the first stage from a regression of the following form: \[ S_i=X\pi_{10}+Z_1\pi_{11}+Z_2\pi_{12}+Z_3\pi_{13}+\eta_1 \] where \(Z_i\) is the dummy for the first three quarters, and \(\pi_i\) is the coefficient on each dummy. Now we look at what they produced in Table 7.2. The coefficients are all negative and significant for the total years of education and the high school graduate dependent variables. Notice, too, that the relationship gets much weaker once we move beyond the groups bound by compulsory schooling: the number of years of schooling for high school students (no effect) and probability of being a college graduate (no effect).

Regarding those college non-results. Ask yourself this question: why should we expect quarter of birth to affect the probability of being a high school graduate but not a college grad? What if we had found quarter of birth predicted high school completion, college completion, post-graduate completion, and total years of schooling beyond high school? Wouldn’t it start to seem like this compulsory schooling instrument was not what we thought it was? After all, this quarter of birth instrument really should only impact high school completion; since it doesn’t bind anyone beyond high school, it shouldn’t affect the number of years beyond high school or college completion probabilities. If it did, we might be skeptical of the whole design. But here it didn’t, which to me makes it even more convincing that they’re identifying a compulsory high school schooling effect.10

Now we look at the second stage for both OLS and 2SLS (which the authors label TSLS, but means the same thing). Table 7.3 shows these results. The authors didn’t report the first stage in this table because they reported it in the earlier table we just reviewed. For small values, the log approximates a percentage change, so they are finding a 7.1% return for every additional year of schooling, but with 2SLS it’s higher (8.9%). That’s interesting, because if it was merely ability bias, then we’d expect the OLS estimate to be too large, not too small. So something other than mere ability bias must be going on here.

| Independent variable | OLS | 2SLS |

|---|---|---|

| Years of schooling | 0.0711 | 0.0891 |

| (0.0003) | (0.0161) | |

| 9 Year-of-birth rummies | Yes | Yes |

| 8 Region-of-residence dummies | No | No |

Standard errors in parenthesis. First stage is quarter of birth dummies.

For whatever it’s worth, I am personally convinced at this point that quarter of birth is a valid instrument and that they’ve identified a causal effect of schooling on earnings, but Angrist and Krueger (1991) want to go further, probably because they want more precision in their estimate. And to get more precision, they load up the first stage with even more instruments. Specifically, they use specifications with 30 dummies (quarter of birth \(\times\) year) and 150 dummies (quarter of birth \(\times\) state) as instruments. The idea is that the quarter of birth effect may differ by state and cohort.

But at what cost? Many of these instruments are only now weakly correlated with schooling—in some locations, they have almost no correlation, and for some cohorts as well. We got a flavor of that, in fact, in Table 7.3, where the later cohorts show less variation in schooling by quarter of birth than the earlier cohorts. What is the effect, then, of reducing the variance in the estimator by loading up the first stage with a bunch of noise?

Bound, Jaeger, and Baker (1995) is a classic work in what is sometimes called the “weak instrument” literature. It’s in this paper that we learn some some very basic problems created by weak instruments, such as the form of 2SLS bias in finite samples. Since Bound, Jaeger, and Baker (1995) focused on the compulsory schooling application that Angrist and Krueger (1991) had done, I will stick with that example throughout. Let’s consider their model with a single endogenous regressor and a simple constant treatment effect. The causal model of interest here is as before: \[ y=\beta s + \varepsilon \] where \(y\) is some outcome and \(s\) is some endogenous regressor, such as schooling. Our instrument is \(Z\) and the first-stage equation is: \[ s=Z' \pi + \eta \] Let’s start off by assuming that \(\varepsilon\) and \(\eta\) are correlated. Then estimating the first equation by OLS would lead to biased results, wherein the OLS bias is: \[ E\big[\widehat{\beta}_{OLS}-\beta\big] = \dfrac{C(\varepsilon, s)}{V(s)} \] We will rename this ratio as \(\dfrac{\sigma_{\varepsilon \eta}}{\sigma^2_s}\). Bound, Jaeger, and Baker (1995) show that the bias of 2SLS centers on the previously defined OLS bias as the weakness of the instrument grows. Following Angrist and Pischke (2009), I’ll express that bias as a function of the first-stage \(F\) statistic: \[ E\big[\widehat{\beta}_{2SLS}-\beta\big] \approx \dfrac{\sigma_{\varepsilon \eta}}{\sigma_\eta^2} \dfrac{1}{F+1} \] where \(F\) is the population analogy of the \(F\)-statistic for the joint significance of the instruments in the first-stage regression. If the first stage is weak, and \(F\rightarrow 0\), then the bias of 2SLS approaches \(\dfrac{\sigma_{\varepsilon \eta}}{\sigma_\eta^2}\). But if the first stage is very strong, \(F \rightarrow \infty\), then the 2SLS bias goes to 0.

Returning to our rhetorical question from earlier, what was the cost of adding instruments without predictive power? Adding more weak instruments causes the first-stage \(F\) statistic to approach zero and increase the bias of 2SLS.

Bound, Jaeger, and Baker (1995) studied this empirically, replicating Angrist and Krueger (1991), and using simulations. Table 7.4 shows what happens once they start adding in controls. Notice that as they do, the \(F\) statistic on the excludability of the instruments falls from 13.5 to 4.7 to 1.6. So by the \(F\) statistic, they are already running into a weak instrument once they include the 30 quarter of birth \(\times\) year dummies, and I think that’s because as we saw, the relationship between quarter of birth and schooling got smaller for the later cohorts.

| Independent variable | OLS | 2SLS | OLS | 2SLS | OLS | 2SLS |

|---|---|---|---|---|---|---|

| Years of schooling | 0.063 | 0.142 | 0.063 | 0.081 | 0.063 | 0.060 |

| (0.000) | (0.033) | (0.000) | (0.016) | (0.000) | (0.029) | |

| First stage \(F\) | 13.5 | 4.8 | 1.6 | |||

| Excluded instruments | ||||||

| Quarter of birth | Yes | Yes | Yes | |||

| Quarter of birth \(\times\) year of birth | No | Yes | Yes | |||

| Number of excluded instruments | 3 | 30 | 28 |

Standard errors in parenthesis. First stage is quarter of birth dummies.

Next, they added in the weak instruments—all 180 of them—which is shown in Table 7.5. And here we see that the problem persists. The instruments are weak, and therefore the bias of the 2SLS coefficient is close to that of the OLS bias.

| Independent variable | OLS | 2SLS | OLS | 2SLS |

|---|---|---|---|---|

| Years of schooling | 0.063 | 0.083 | 0.063 | 0.081 |

| (0.000) | (0.009) | (0.000) | (0.011) | |

| First stage \(F\) | 2.4 | 1.9 | ||

| Excluded instruments | ||||

| Quarter of birth | Yes | Yes | ||

| Quarter of birth \(\times\) year of birth | Yes | Yes | ||

| Quarter of birth \(\times\) state of birth | Yes | Yes | ||

| Number of excluded instruments | 180 | 178 |

Standard errors in parenthesis.

But the really damning part of the Bound, Jaeger, and Baker (1995) was their simulation. The authors write:

To illustrate that second-stage results do not give us any indication of the existence of quantitatively important finite-sample biases, we reestimated Table 1, columns (4) and (6) and Table 2, columns (2) and (4), using randomly generated information in place of the actual quarter of birth, following a suggestion by Alan Krueger. The means of the estimated standard errors reporting in the last row are quite close to the actual standard deviations of the 500 estimates for each model. . . . It is striking that the second-stage results reported in Table 3 look quite reasonable even with no information about educational attainment in the simulated instruments. They give no indication that the instruments were randomly generated\(\ldots\) On the other hand, the F statistics on the excluded instruments in the first-stage regressions are always near their expected value of essentially 1 and do give a clear indication that the estimates of the second-stage coefficients suffer from finite-sample biases. Bound, Jaeger, and Baker (1995) (p.448)

So, what can you do if you have weak instruments? Unfortunately, not a lot. You can use a just-identified model with your strongest IV. Second, you can use a limited-information maximum likelihood estimator (LIML). This is approximately median unbiased for over identified constant effects models. It provides the same asymptotic distribution as 2SLS under homogeneous treatment effects but provides a finite-sample bias reduction.

But, let’s be real for a second. If you have a weak instrument problem, then you only get so far by using LIML or estimating a just-identified model. The real solution for a weak instrument problem is to get better instruments. Under homogeneous treatment effects, you’re always identifying the same effect, so there’s no worry about a complier only parameter. So you should just continue searching for stronger instruments that simultaneously satisfy the exclusion restriction.11

In conclusion, I think we’ve learned a lot about instrumental variables and why they are so powerful. The estimators based on this design are capable of identifying causal effects when your data suffer from selection on unobservables. Since selection on unobservables is believed to be very common, this is a very useful methodology for addressing that. But, that said, we also have learned some of the design’s weaknesses, and hence why some people eschew it. Let’s now move to heterogeneous treatment effects so that we can better understand some limitations a bit better.

Now we turn to a scenario where we relax the assumption that treatment effects are the same for every unit. This is where the potential outcomes notation comes in handy. Instead, we will allow for each unit to have a unique response to the treatment, or \[ Y_i^1 - Y_i^0 = \delta_i \] Note that the treatment effect parameter now differs by individual \(i\). We call this heterogeneous treatment effects.

The main questions we have now are: (1) what is IV estimating when we have heterogeneous treatment effects, and (2) under what assumptions will IV identify a causal effect with heterogeneous treatment effects? The reason this matters is that once we introduce heterogeneous treatment effects, we introduce a distinction between the internal validity of a study and its external validity. Internal validity means our strategy identified a causal effect for the population we studied. But external validity means the study’s finding applied to different populations (not in the study). The deal is that under homogeneous treatment effects, there is no tension between external and internal validity because everyone has the same treatment effect. But under heterogeneous treatment effects, there is huge tension; the tension is so great, in fact, that it may even undermine the meaningfulness of the relevance of the estimated causal effect despite an otherwise valid IV design!12

Heterogeneous treatment effects are built on top of the potential outcomes notation, with a few modifications. Since now we have two arguments—\(D\) and \(Z\)—we have to modify the notation slightly. We say that \(Y\) is a function of \(D\) and \(Z\) as \(Y_i(D_i=0,Z_i=1)\), which is represented as \(Y_i(0,1)\).

Potential outcomes as we have been using the term refers to the \(Y\) variable, but now we have a new potential variable—potential treatment status (as opposed to observed treatment status). Here are the characteristics:

\[ \begin{align} D_i^1 & =i\text{'s treatment status when }Z_i=1 \\ D_i^0 & =i\text{'s treatment status when }Z_i=0 \end{align} \]

And observed treatment status is based on a treatment status switching equations:

\[ \begin{align} D_i &=&D_i^0 + (D_i^1 - D_i^0)Z_i \\ &=&\pi_0 + \pi_1 Z_i + \phi_i \end{align} \]

where \(\pi_{0i}=E[D_i^0]\), \(\pi_{1i} = (D_i^1 - D_i^0)\) is the heterogeneous causal effect of the IV on \(D_i\), and \(E[\pi_{1i}]=\) the average causal effect of \(Z_i\) on \(D_i\).

There are considerably more assumptions necessary for identification once we introduce heterogeneous treatment effects—specifically five assumptions. We now review each of them. And to be concrete, I use repeatedly as an example the effect of military service on earnings using a draft lottery as the instrumental variable (Angrist 1990). In that paper, Angrist estimated the returns to military service using as an instrument the person’s draft lottery number. The draft lottery number was generated by a random number generator and if a person’s number was in a particular range, they were drafted, otherwise they weren’t.

First, as before, there is a stable unit treatment value assumption (SUTVA) that states that the potential outcomes for each person \(i\) are unrelated to the treatment status of other individuals. The assumption states that if \(Z_i=Z_i'\), then \(D_i(Z) = D_i(Z')\). And if \(Z_i=Z_i'\) and \(D_i=D_i'\), then \(Y_i(D,Z)=Y_i(D',Z')\). A violation of SUTVA would be if the status of a person at risk of being drafted was affected by the draft status of others at risk of being drafted. Such spillovers violate SUTVA.13 Not knowing a lot about how that works, I can’t say whether Angrist’s draft study would’ve violated SUTVA. But it seems like he’s safe to me.

Second, there is the independence assumption. The independence assumption is also sometimes called the “as good as random assignment” assumption. It states that the IV is independent of the potential outcomes and potential treatment assignments. Notationally, it is \[ \Big\{Y_i(D_i^1,1), Y_i(D_i^0,0),D_i^1,D_i^0\Big\} \independent Z_i \] The independence assumption is sufficient for a causal interpretation of the reduced form:

\[ \begin{align} E\big[Y_i\mid Z_i=1\big]-E\big[Y_i\mid Z_i=0\big] & = E\big[Y_i(D_i^1,1)\mid Z_i=1\mid]- E\big[Y_i(D_i^0,0)\mid Z_i=0\big] \\ & = E[Y_i(D_i^1,1)] - E[Y_i(D_i^0,0)] \end{align} \]

And many people may actually prefer to work just with the instrument and its reduced form because they find independence satisfying and acceptable. The problem, though, is technically the instrument is not the program you’re interested in studying. And there may be many mechanisms leading from the instrument to the outcome that you need to think about (as we will see below). Ultimately, independence is nothing more and nothing less than assuming that the instrument itself is random.

Independence means that the first stage measures the causal effect of \(Z_i\) on \(D_i\):

\[ \begin{align} E\big[D_i\mid Z_i=1\big]-E\big[D_i\mid Z_i=0\big] & = E\big[D_i^1\mid Z_i=1\big] - E\big[D_i^0\mid Z_i=0\big] \\ & = E[D_i^1 - D_i^0] \end{align} \]

An example of this is if Vietnam conscription for military service was based on randomly generated draft lottery numbers. The assignment of draft lottery number was independent of potential earnings or potential military service because it was “as good as random.”

Third, there is the exclusion restriction. The exclusion restriction states that any effect of \(Z\) on \(Y\) must be via the effect of \(Z\) on \(D\). In other words, \(Y_i(D_i,Z_i)\) is a function of \(D_i\) only. Or formally: \[ Y_i(D_i,0) = Y_i(D_i,1)\quad \text{for $D=0,1$} \] Again, our Vietnam example. In the Vietnam draft lottery, an individual’s earnings potential as a veteran or a non-veteran are assumed to be the same regardless of draft eligibility status. The exclusion restriction would be violated if low lottery numbers affected schooling by people avoiding the draft. If this was the case, then the lottery number would be correlated with earnings for at least two cases. One, through the instrument’s effect on military service. And two, through the instrument’s effect on schooling. The implication of the exclusion restriction is that a random lottery number (independence) does not therefore imply that the exclusion restriction is satisfied. These are different assumptions.

Fourth is the first stage. IV designs require that \(Z\) be correlated with the endogenous variable such that \[ E[D_i^1 - D_i^0] \ne 0 \] \(Z\) has to have some statistically significant effect on the average probability of treatment. An example would be having a low lottery number. Does it increase the average probability of military service? If so, then it satisfies the first stage requirement. Note, unlike independence and exclusion, the first stage is testable as it is based solely on \(D\) and \(Z\), both of which you have data on.

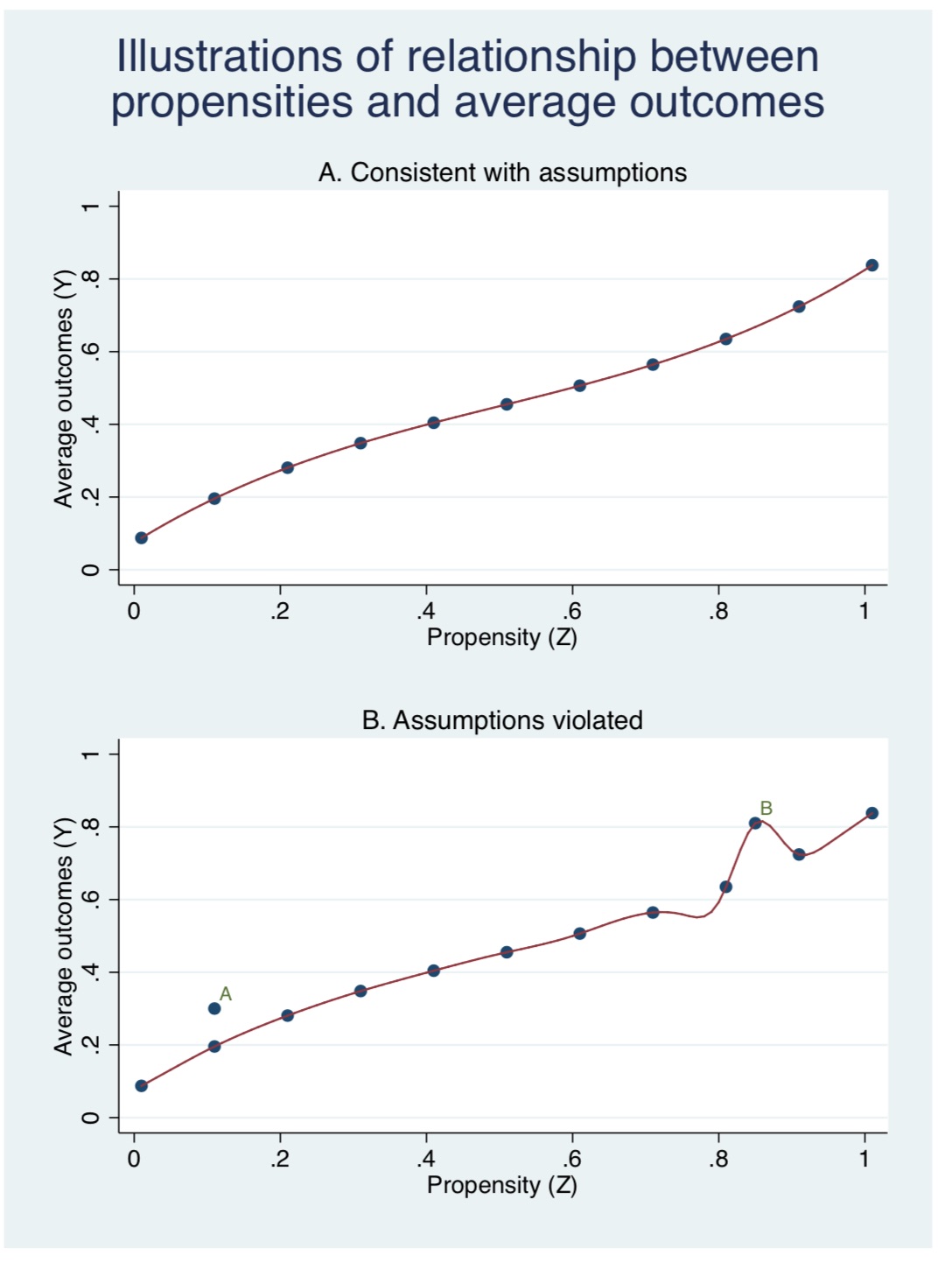

And finally, there is the monotonicity assumption. This is only strange at first glance but is actually quite intuitive. Monotonicity requires that the instrumental variable (weakly) operate in the same direction on all individual units. In other words, while the instrument may have no effect on some people, all those who are affected are affected in the same direction (i.e., positively or negatively, but not both). We write it out like this: \[ \text{Either $\pi_{1i} \geq 0$ for all $i$ or $\pi_{1i} \leq 0$ for all $i=1,\dots, N$} \] What this means, using our military draft example, is that draft eligibility may have no effect on the probability of military service for some people, like patriots, people who love and want to serve their country in the military, but when it does have an effect, it shifts them all into service, or out of service, but not both. The reason we have to make this assumption is that without monotonicity, IV estimators are not guaranteed to estimate a weighted average of the underlying causal effects of the affected group.

If all five assumptions are satisfied, then we have a valid IV strategy. But that being said, while valid, it is not doing what it was doing when we had homogeneous treatment effects. What, then, is the IV strategy estimating under heterogeneous treatment effects? Answer: the local average treatment effect (LATE) of \(D\) on \(Y\):

\[ \begin{align} \delta_{IV,LATE} & =\dfrac{ \text{Effect of $Z$ on $Y$}}{\text{Effect of $Z$ on $D$}} \\ & =\dfrac{E\big[Y_i(D_i^1,1)-Y_i(D_i^0,0)\big]}{ E[D_i^1 - D_i^0]} \\ & =E\big[(Y_i^1-Y_i^0)\mid D_i^1-D_i^0=1\big] \end{align} \]

The LATE parameter is the average causal effect of \(D\) on \(Y\) for those whose treatment status was changed by the instrument, \(Z\). We know that because notice the difference in the last line: \(D_i^1 - D_i^0\). So, for those people for whom that is equal to 1, we calculate the difference in potential outcomes. Which means we are only averaging over treatment effects for whom \(D_i^1 - D_i^0\). Hence why the parameter we are estimating is “local.”

How do we interpret Angrist’s estimated causal effect in his Vietnam draft project? Well, IV estimates the average effect of military service on earnings for the subpopulations who enrolled in military service because of the draft. These are specifically only those people, though, who would not have served otherwise. It doesn’t identify the causal effect on patriots who always serve, for instance, because \(D_i^1 - D_i^0 = 0\) for patriots. They always serve! \(D_i^1=1\) and \(D_i^0=1\) for patriots because they’re patriots! It also won’t tell us the effect of military service on those who were exempted from military service for medical reasons because for these people \(D_i^1=0\) and \(D_i^0=0\).14

The LATE framework has even more jargon, so let’s review it now. The LATE framework partitions the population of units with an instrument into potentially four mutually exclusive groups. Those groups are:

Compliers: This is the subpopulation whose treatment status is affected by the instrument in the correct direction. That is, \(D_i^1=1\) and \(D_i^0=0\).

Defiers: This is the subpopulation whose treatment status is affected by the instrument in the wrong direction. That is, \(D_i^1=0\) and \(D_i^0=1\).15

Never takers: This is the subpopulation of units that never take the treatment regardless of the value of the instrument. So, \(D_i^1=D_i^0=0\). They simply never take the treatment.16

Always takers: This is the subpopulation of units that always take the treatment regardless of the value of the instrument. So, \(D_i^1=D_i^0=1\). They simply always take the instrument.17

As outlined above, with all five assumptions satisfied, IV estimates the average treatment effect for compliers, which is the parameter we’ve called the local average treatment effect. It’s local in the sense that it is average treatment effect to the compliers only. Contrast this with the traditional IV pedagogy with homogeneous treatment effects. In that situation, compliers have the same treatment effects as non-compliers, so the distinction is irrelevant. Without further assumptions, LATE is not informative about effects on never-takers or always-takers because the instrument does not affect their treatment status.

Does this matter? Yes, absolutely. It matters because in most applications, we would be mostly interested in estimating the average treatment effect on the whole population, but that’s not usually possible with IV.18

Now that we have reviewed the basic idea and mechanics of instrumental variables, including some of the more important tests associated with it, let’s get our hands dirty with some data. We’ll work with a couple of data sets now to help you better understand how to implement 2SLS in real data.

Buy the print version today:

We will once again look at the returns to schooling since it is such a historically popular topic for causal questions in labor. In this application, we will simply estimate a 2SLS model, calculate the first-stage F statistic, and compare the 2SLS results with the OLS results. I will be keeping it simple, because my goal is just to help the reader become familiarized with the procedure.

The data comes from the NLS Young Men Cohort of the National Longitudinal Survey. This data began in 1966 with 5,525 men aged 14–24 and continued to follow up with them through 1981. These data come from 1966, the baseline survey, and there are a number of questions related to local labor-markets. One of them is whether the respondent lives in the same county as a 4-year (and a 2-year) college.

Card (1995) is interested in estimating the following regression equation: \[ Y_i=\alpha+\delta S_i + \gamma X_i+\varepsilon_i \] where \(Y\) is log earnings, \(S\) is years of schooling, \(X\) is a matrix of exogenous covariates, and \(\varepsilon\) is an error term that contains, among other things, unobserved ability. Under the assumption that \(\varepsilon\) contains ability, and ability is correlated with schooling, then \(C(S,\varepsilon)\neq 0\) and therefore schooling is biased. Card (1995) proposes therefore an instrumental variables strategy whereby he will instrument for schooling with the college-in-the-county dummy variable.

It is worth asking ourselves why the presence of a 4-year college in one’s county would increase schooling. The main reason I can think of is that the presence of the 4-year college increases the likelihood of going to college by lowering the costs, since the student can live at home. This therefore means that we are selecting on a group of compliers whose behavior is affected by the variable. Some kids, in other words, will always go to college regardless of whether a college is in their county, and some will never go despite the presence of the nearby college. But there may exist a group of compliers who go to college only because their county has a college, and if I’m right that this is primarily picking up people going because they can attend while living at home, then it’s necessarily people at some margin who attend only because college became slightly cheaper. This is, in other words, a group of people who are liquidity constrained. And if we believe the returns to schooling for this group are different from those of the always-takers, then our estimates may not represent the ATE. Rather, they would represent the LATE. But in this case, that might actually be an interesting parameter since it gets at the issue of lowering costs of attendance for poorer families.

Here we will do some simple analysis based on Card (1995).

use https://github.com/scunning1975/mixtape/raw/master/card.dta, clear

* OLS estimate of schooling (educ) on log wages

reg lwage educ exper black south married smsa

* 2SLS estimate of schooling (educ) on log wages using "college in the county" as an instrument for schooling

ivregress 2sls lwage (educ=nearc4) exper black south married smsa, first

* First stage regression of schooling (educ) on all covariates and the college and the county variable

reg educ nearc4 exper black south married smsa

* F test on the excludability of college in the county from the first stage regression.

test nearc4library(AER)

library(haven)

library(tidyverse)

read_data <- function(df)

{

full_path <- paste("https://github.com/scunning1975/mixtape/raw/master/",

df, sep = "")

df <- read_dta(full_path)

return(df)

}

card <- read_data("card.dta")

#Define variable

#(Y1 = Dependent Variable, Y2 = endogenous variable, X1 = exogenous variable, X2 = Instrument)

attach(card)

Y1 <- lwage

Y2 <- educ

X1 <- cbind(exper, black, south, married, smsa)

X2 <- nearc4

#OLS

ols_reg <- lm(Y1 ~ Y2 + X1)

summary(ols_reg)

#2SLS

iv_reg = ivreg(Y1 ~ Y2 + X1 | X1 + X2)

summary(iv_reg)import numpy as np

import pandas as pd

import statsmodels.api as sm

import statsmodels.formula.api as smf

from itertools import combinations

import plotnine as p

# read data

import ssl

ssl._create_default_https_context = ssl._create_unverified_context

def read_data(file):

return pd.read_stata("https://github.com/scunning1975/mixtape/raw/master/" + file)

card = read_data("card.dta")

#OLS

ols_reg = sm.OLS.from_formula("lwage ~ educ + exper + black + south + married + smsa",

data = card).fit()

ols_reg.summary()

#2SLS

iv_reg = IV2SLS.from_formula("lwage ~ 1 + exper + black + south + married + smsa + [educ ~ nearc4 ]", card).fit()

iv_reg.summaryOur results from this analysis have been arranged into Table 7.6. First, we report our OLS results. For every one year additional of schooling, respondents’ earnings increase by approximately 7.1%. Next we estimated 2SLS using the ivregress 2sls command in Stata. Here we find a much larger return to schooling than we had found using OLS—around 75% larger in fact. But let’s look at the first stage. We find that the college in the county is associated with 0.327 more years of schooling. This is highly significant (\(p<0.001\)). The \(F\) statistic exceeds 15, suggesting we don’t have a weak instrument problem. The return to schooling associated with this 2SLS estimate is 0.124—that is, for every additional year of schooling, earnings increase by 12.4%. Other covariates are listed if you’re interested in studying them as well.

| Dependent variable | OLS | 2SLS |

| educ | \(0.071^{***}\) | 0.124\(^{**}\) |

| (0.003) | (0.050) | |

| exper | \(0.034^{***}\) | 0.056\(^{***}\) |

| (0.002) | (0.020) | |

| black | \(-0.166^{***}\) | \(-0.116^{**}\) |

| (0.018) | (0.051) | |

| south | \(-0.132^{***}\) | \(-0.113^{***}\) |

| (0.015) | (0.023) | |

| married | \(-0.036^{***}\) | \(-0.032^{***}\) |

| (0.003) | (0.005) | |

| smsa | \(0.176^{***}\) | \(0.148^{***}\) |

| (0.015) | (0.031) | |

| First Stage Instrument | ||

| College in the county | 0.327\(^{***}\) | |

| Robust standard error | (0.082) | |

| F statistic for IV in first stage | 15.767 | |

| N | 3,003 | 3,003 |

| Mean Dependent Variable | 6.262 | 6.262 |

| Std. Dev. Dependent Variable | 0.444 | 0.444 |

Standard errors in parenthesis. \(^{*}\) \(p<0.10\), \(^{**}\) \(p<0.05\), \(^{***}\) \(p<0.01\)

Why would the return to schooling be so much larger for the compliers than for the general population? After all, we showed earlier that if this was simply ability bias, then we’d expect the 2SLS coefficient to be smaller than the OLS coefficient, because ability bias implies that the coefficient on schooling is too large. Yet we’re finding the opposite. So a couple of things it could be. First, it could be that schooling has measurement error. Measurement error would bias the coefficient toward zero, and 2SLS would recover its true value. But I find this explanation to be unlikely, because I don’t foresee people really not knowing with accuracy how many years of schooling they currently have. Which leads us to the other explanation, and that is that compliers have larger returns to schooling. But why would this be the case? Assuming that the exclusion restriction holds, then why would compliers, returns be so much larger? We’ve already established that these people are likely being shifted into more schooling because they live with their parents, which suggests that the college is lowering the marginal cost of going to college. All we are left saying is that for some reason, the higher marginal cost of attending college is causing these people to underinvest in schooling; that in fact their returns are much higher.

The second exercise that we’ll be doing is based on Graddy (2006). My understanding is that Graddy collected these data herself by recording prices of fish at the actual Fulton Fish Market. I’m not sure if that is true, but I like to believe it’s true. Anyhow, the Fulton Fish Market operated in New York on Fulton Street for 150 years. In November 2005, it moved from Lower Manhattan to a large facility building for the market in the South Bronx. At the time when Graddy (2006) was published, the market was called the New Fulton Fish Market. It’s one of the world’s largest fish markets, second only to the Tsukiji in Tokyo.